آخر المواضيع المضافة

تاريخ الرياضيات

الرياضيات في الحضارات المختلفة

الرياضيات المتقطعة

الجبر

الهندسة

المعادلات التفاضلية و التكاملية

التحليل

علماء الرياضيات

تاريخ الرياضيات

الرياضيات في الحضارات المختلفة

الرياضيات المتقطعة

الجبر

الهندسة

المعادلات التفاضلية و التكاملية

التحليل

علماء الرياضيات | Martingale |

|

|

Read More

Date: 19-2-2021

Date: 29-3-2021

Date: 16-4-2021

|

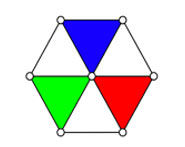

A sequence of random variates  ,

,  , ... with finite means such that the conditional expectation of

, ... with finite means such that the conditional expectation of  given

given  ,

,  ,

,  , ...,

, ...,  is equal to

is equal to  , i.e.,

, i.e.,

|

(Feller 1971, p. 210). The term was first used to describe a type of wagering in which the bet is doubled or halved after a loss or win, respectively. The concept of martingales is due to Lévy, and it was developed extensively by Doob.

A one-dimensional random walk with steps equally likely in either direction ( ) is an example of a martingale.

) is an example of a martingale.

REFERENCES:

Doob, J. L. Stochastic Processes. New York: Wiley, 1953.

Feller, W. "Martingales." §6.12 in An Introduction to Probability Theory and Its Applications, Vol. 2, 3rd ed. New York: Wiley, pp. 210-215, 1971.

Lévy, P. Calcul de probabilités. Paris: Gauthier-Villars, 1925.

Lévy, P. Théorie de l'addition des variables aléatoires. Paris: Gauthier-Villars, 1954.

Lévy, P. Processus stochastiques et mouvement Brownien, 2nd ed. Paris: Gauthier-Villars, 1965.

Loève, M. Probability Theory I, 4th ed. New York: Springer-Verlag, 1977.

|

|

|

|

دخلت غرفة فنسيت ماذا تريد من داخلها.. خبير يفسر الحالة

|

|

|

|

|

|

|

ثورة طبية.. ابتكار أصغر جهاز لتنظيم ضربات القلب في العالم

|

|

|

|

|

|

|

سماحة السيد الصافي يؤكد ضرورة تعريف المجتمعات بأهمية مبادئ أهل البيت (عليهم السلام) في إيجاد حلول للمشاكل الاجتماعية

|

|

|